Sergei Chayko/iStock via Getty Images

Let’s put short-term events aside for a second here and focus on the bigger, longer-term picture of the oil market. Russia is the world’s second largest oil producer. Even before the invasion of Ukraine, Russia’s oil production was is expected to peak due to lack of investment in the period 2014-2019.

This was detailed in a Oxford Institute for Energy Studies article.

Oxford Institute for Energy Studies

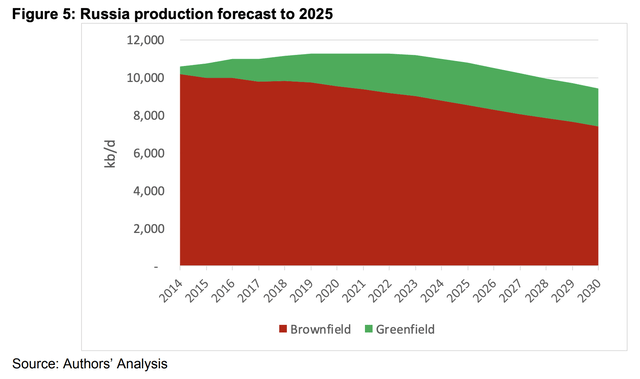

In the graph above, Brownfield is the production currently in progress, while Greenfield is the production that should start. Since writing this article in 2019, we are already at the peak of Russian oil production. After the 2020 price war, where Saudi Arabia specifically targeted the shutdown of Russian oil production, there was a significant impact on Russia’s total capacity. We estimate Russia’s peak capacity at around ~11.1m bpd versus around 11.9m bpd previously.

Now that the West is sanctioning the Russian financial system and the service companies are pulling out and capital is being limited (by the departure of the oil majors), what will happen to Russian oil production in the future?

Oxford Institute for Energy Studies

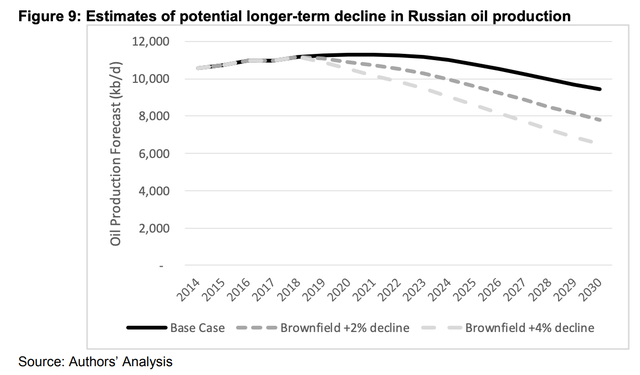

Here is the author’s analysis, assuming a constant rate of decline of 2% and 4%. Even in the base scenario, Russia’s oil production was expected to peak this year and gradually fall through 2030. With the situation just outlined above, there is a good chance that oil production of Russia is approaching the 4% decline rate scenario.

This puts a rather interesting scenario in our hands. Even if China and India are intervening in the short term to combat the possible decline in Russian crude exports, the longer term situation is the same. Without capex investment in Russian oilfields, the decline will become steep and total capacity will decrease.

Oxford Institute for Energy Studies

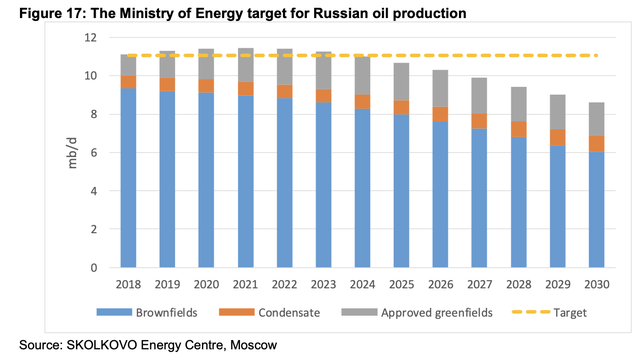

While Moscow is setting itself a long-term target of around 11 million bpd, new projects approved through 2019 have not been enough to keep production flat. This scenario was probably exacerbated after the invasion of Ukraine.

What does this mean for global oil supply and demand?

I need you to sit somewhere quiet now and think about this. I’m going to lay out the scenarios, and you have to come to your own conclusion.

The current oil market deficit is around 2 million bpd. If you want to be conservative, let’s call it ~1 million bpd.

Growth in oil demand from 2022 to 2030: ~6 to ~7 million bpd.

Growth in US oil production from 2022 to 2030: 2 to 3 million b/d.

Unused capacity OPEC+: 1.5 million bpd.

Iran: 1.4 million bpd.

Canada: 500,000 bpd.

Russia: -3 million b/d.

Non-OPEC production outside the US: -2 million bpd.

Report: -6.4 million bpd.

I don’t know about you, but in terms of headroom, that’s a pretty big cushion. The key number in all of this is demand growth, and so unless you expect the global economy to go into recession for 8 years, we think the likelihood of demand reaching 108 to 110 million b/d is very plausible.

As you can see, the odds are heavily skewed in favor of a structural oil market deficit on the horizon. You can slice and dice this scan however you like, but the result is the same. We are heading towards a structural shortage of oil supply. And with Russia already experiencing a peak in oil production before this invasion of Ukraine, the current decline will only get worse.

If you need time to tell yourself we’re still in Round 2, do it now. As you can see, once the deficit is running, only demand destruction can balance the market.

More Stories

🌱 Rail In Roanoke Fifth Anniversary + ‘Love Letters’ Production

Industrial production in South Korea contracts by 1.8% in September

PM Modi lays foundation stone for C-295 transport aircraft production plant